Three Bubbles, One Cycle: Fred Harrison on the Crash That’s Already Under Way

The Bubbles Are Already Bursting. Land, SpaceX, Carbon. And Governments Can't Stop Any of Them.

Last week’s conversation with Fred Harrison landed harder than almost anything I have published on this Substack. Tens of thousands of people watched or read it. The messages I received made clear that people are frightened, that they recognise something in what Fred is describing, even if they cannot yet put a name to it. So we spoke again. What follows is my account of that second conversation, and it is, if anything, grimmer than the first.

Fred wanted to begin not with Elon Musk, who was the question I opened with, but with the housing market. He had something to say first, and he was right to insist on it.

A Rerun, With Extras

Cast your mind back to the early 2000s. Mortgages were being sold to people who could not afford them: subprime loans, packaged up and sold on to pension funds and local councils. When the market blew up in 2008, the institutions holding those packages found themselves effectively bankrupt. Governments stepped in with emergency loans. National debt ballooned. The burden of that debt fell on ordinary people, who spent the next ten years paying for a crisis they did not create.

Fred’s opening point was simple: exactly the same thing is happening now, with a new mechanism layered on top of it.

The new mechanism is the so-called borrow-now-pay-later loan. These products are being sold to people who cannot afford their mortgages. The logic runs like this. You take out a mortgage you cannot quite sustain. Then you borrow from a separate lender on a borrow-now-pay-later basis, using that loan to cover the mortgage payments. Instead of paying a full monthly mortgage, you stagger the payments fortnightly or weekly, drawing down the loan to bridge the gap each time. You are not solving a cash-flow problem. You are deepening it, week by week.

These borrow-now-pay-later loans are then being packaged into collateralised instruments and sold on to pension funds and student loan companies, in a direct echo of what happened with subprime mortgages before 2008.

But here is the crucial difference. Before 2008, the bust caught homebuyers. Renters were largely outside the blast radius. This time they are inside it. People living on thin margins, with no savings beyond three weeks of expenses, are using borrow-now-pay-later products to pay their rent. Not to buy. Just to pay the rent they already owe. When the market turns, they will not simply lose a home they own. They will find themselves unable to meet rent commitments while simultaneously servicing loans they took out to meet those same commitments. They will have nothing to fall back on.

Fred was unambiguous about the scale. The property market in both the United States and the United Kingdom is, in his words, “absolutely vulnerable to millions of people.” The credit agencies are not disclosing how fragile these loan books are. The regulatory bodies that are supposed to be watching the market are largely ignorant of what is happening beneath the surface. When one institution cracks, the contagion will move fast and the authorities will be caught flat-footed, as they were before.

What Musk Is Actually Selling

I asked Fred about Elon Musk. The SpaceX valuation is now somewhere north of a trillion dollars. People are talking about Musk becoming the world’s first trillionaire. Fred’s analysis of that figure is not about Musk the entrepreneur. It is about what the valuation actually represents.

What makes Starlink valuable? Not the satellites themselves, not the engineering, not the brand. What makes it valuable is access to the electromagnetic spectrum: the band of natural resource that connects the Earth’s surface to near-orbit. That is not a product Musk created. It is a natural resource that he has been given, effectively, for free. Classical economists, from Adam Smith onwards, have always defined “land” not merely as the surface of the earth, but as all natural resources, including spectrum, airspace, and whatever lies beyond it.

So when people rush into SpaceX stock, they are, without knowing it, speculating on a land price. The trillion-dollar valuation is a capitalisation of access to a natural resource. It is the same mechanism as a rising house price, or a rising rent, translated into space.

Fred’s conclusion follows directly. Prices have been rising. Investors assume the trend continues. They pour money into Musk’s companies despite the absence of profit, expecting to cash out on the rising valuation. When somebody rings the alarm bell, as they always do at the end of a cycle, everyone will want to exit at once, and the stampede will cause the very collapse they were rushing to avoid.

Whether you are looking at earth or the heavens, the analysis is the same. Speculation on a stream of income that lies beyond democratic control or public regulation. The 18-year cycle will take it from here.

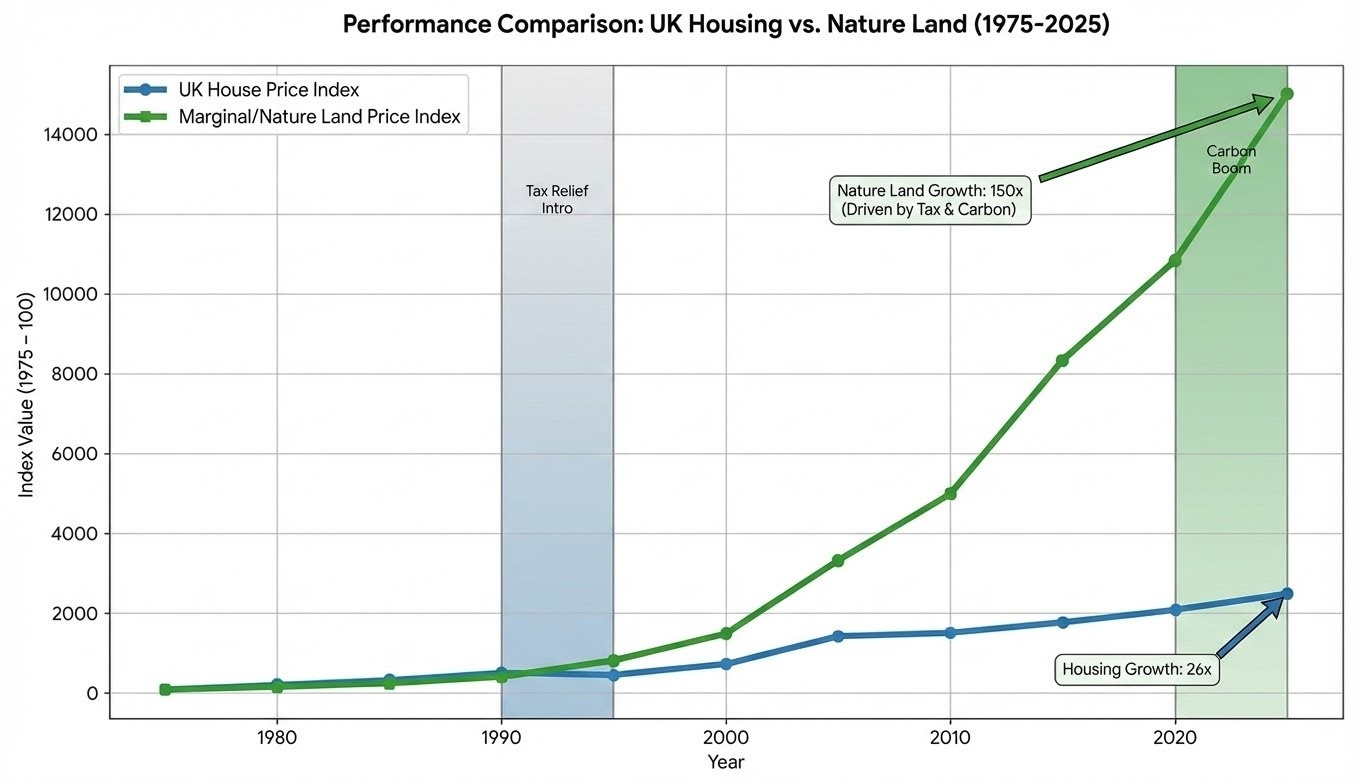

Scotland’s Frozen Fields

I mentioned to Fred something I had been researching for a separate piece: the carbon credit bubble, and what it has done to rural land prices in Scotland.

The report from the Scottish Government land agents tells a stark story. In the period running up to last Christmas, the most unproductive land in Scotland, hillside that cannot be farmed, was changing hands at up to £14,000 an acre. Buyers were purchasing it for carbon credits: the expectation that society would pay them to store carbon in trees planted on otherwise worthless ground. Then, suddenly, the market froze. Not fell. Froze. The price is not low. There are simply no buyers. The agents have nothing to report.

Rural Land Market Insights Report

https://www.landcommission.gov.scot/downloads/Rural-Land-Market-Insights-Report-2026.pdf

I described this to Fred as a live laboratory for what is coming in other markets. He agreed immediately. The carbon credit market inflated on the back of government subsidies. When investors began to sense that governments could not sustain those subsidies indefinitely, given the scale of public debt already accumulated, money started leaving. The speculative logic collapsed because it depended entirely on a promise that the state can no longer credibly make.

There is a further layer to this particular fraud. The trees being planted to sequester carbon are, in many cases, poor-quality commercial forestry: they destroy the soil structure beneath them and release carbon dioxide into the atmosphere rather than storing it. The scientific premise of the credit is faulty. The financial premise has now also been punctured. What is left is frozen ground and frozen order books.

Fred added a broader point. Investors who entered the carbon market when the subsidies were flowing are now showing extreme caution. Some are pulling money towards other speculative vehicles. Others are pulling out of speculation altogether, recognising that governments cannot keep underwriting the cycle’s later stages. The whole system is primed for a single large shock to set it off, and nobody can say with certainty what that shock will be.

In the last cycle, it was a bank going under. It could be that again. It could be something eccentric from Washington. Fred’s phrase was direct: “We are sitting ducks waiting for something bad to happen.”

Governments Have No Firepower Left

This was the part of the conversation that stayed with me most after we finished.

I mentioned that earlier in the day I had been on a conference call with people from the environment agency and water company representatives. One of the people on that call said something I have been thinking about since. It does not matter, he said, whether the water companies are nationalised or not. The money has been spent. The debt is too large. No government can borrow what would be needed to repair the decades of underinvestment and negligence in the water infrastructure. We are going to have worse water quality and worse sewage management for years to come, possibly decades.

You can see it in the roads. You can feel it in the fabric of daily life. Broken Britain is not a metaphor. It is a description of a country that has been running down its physical stock for a generation and now lacks the fiscal capacity to reverse the decline.

Fred widened the lens. This is not only Britain. In the United States, rising sea levels are already displacing coastal communities. The infrastructure required to move those communities inland does not yet exist. The cost of building it is enormous. When it is built, it will push up property prices in the inland areas receiving those communities, adding another layer of housing stress to a market already under severe strain. A feedback loop: disaster compounds disaster, and governments are not thinking clearly about how to navigate any of it.

And when the economy turns down in earnest, governments in the United States and the United Kingdom will find themselves unable to borrow at the scale they managed in 2008. The private sector will not lend to governments it judges incapable of repayment. The safety net that caught people last time will not be there this time.

Fred did not need to spell out the political consequences. Economic desperation at scale, combined with an inability to respond from the centre, is precisely the condition that adventurous authoritarians exploit. The Putins and the Irans of the world will read Western vulnerability and act accordingly.

The AI Wildcard

There was one element Fred raised that I want to set out separately, because it has not been sufficiently integrated into most discussions of what is coming.

Low-income renters using borrow-now-pay-later products to meet their weekly rent are the most exposed people in this picture. They have no savings cushion, no property asset, and growing personal debt. They are entirely dependent on their income continuing.

Fred’s observation was this: many of those same people are about to lose their jobs to automation. The AI displacement of low-skill and mid-skill employment is not a future risk. It is a current process. When those jobs go, the income stream that was already failing to cover rent without borrowed supplementation will simply stop. The loans will turn immediately unserviceable. The rent arrears will follow. And the government, as we have just established, will not have the resources to catch them.

This is the convergence Fred has been predicting. Not one crisis, but several crises arriving at roughly the same point in the cycle, reinforcing each other, and finding a public sector too exhausted and too indebted to mount an effective response.

There Is a Solution, But You Won’t Hear It in Westminster or Washington

Fred will be the first to say that this is not a counsel of despair, and I want to be faithful to that.

There is a reform that would change the picture. It has been available for 250 years, since Adam Smith set it out in the foundational texts of political economy, developed through Ricardo and Mill and given its clearest popular expression by Henry George. The reform is the restructuring of government revenue: shifting the tax base away from wages and enterprise, towards the capture of economic rents, the unearned gains that accrue to land and natural resource holders simply because society exists and grows around them.

If governments captured those rents publicly, several things would follow. Ordinary people would be liberated from the tax burden that currently suppresses their wages and discourages productive activity. Productivity would rise. New revenue would flow, not borrowed, not taxed from income, but drawn from the wealth that is currently being privatised by landowners and speculators. With that revenue, it would be possible to fund the coastal relocations, the water infrastructure, the transition through the disruption ahead.

Fred is not naive about the difficulty. The interests that benefit from the current system are powerful and well-organised. The information that would lead people to demand reform is systematically withheld, not by conspiracy but by the structural tendency of elite institutions to ignore ideas that threaten elite interests. The solution has been sitting in the economic literature for two and a half centuries. It has not been implemented because those who would lose from it have never allowed it to become politically legible.

That is the work. Not to discover the answer: it is already there. The work is to make it impossible to ignore.

Fred put it plainly at the end of our conversation. People should not despair. Being informed is not the same as being powerless. There is a route through what is coming, but it requires people to understand the system well enough to demand that it change.

A Note on Fred’s Book

The blueprint Fred is describing is set out in his recent book, Cheating. It is not a quick read and it should not be. The argument is serious and the evidence is extensive. If you want to understand not just what is wrong but how it could be different, that is where to start.

We will continue this conversation.

Fred Harrison’s book Cheating lays out the full argument. Read it. Fred Harrison’s book Cheating is available now: https://shepheardwalwyn.com/product/cheating-the-human-project-and-its-betrayal/

And follow this Substack, because this conversation is far from over.

What governments can charge Musk a fair rent for the spectrum?

Worrying stuff Peter. I am not an economist but a Project Engineer/Manager/Consultant and usually have to read these economic articles at least twice.

One of the things resulting from 40 years of running complex projects is to ask the simple questions no one else will ask. So please bear with me as I frame my question.

Given that many countries are inefficient in use of resources and of peoples efforts with their convoluted economies hindering the ability to maximise benefit to society.

In my project management consultancy we regularly take diagonal slices of various teams and ask them to put aside preconceptions and current limitations and to generate a “View of perfection” for that process. Whilst perfection is not feasible this exercise provides stepping stones towards significant process improvement and empowers the teams to move forward.

Be interested to hear what your unfettered “View of perfection” would be.